The positive impact of platforms on conversion and retention rates (Session 4/5)

5min

The positive impact of platforms on conversion and retention rates (Session 4/5)

In this section we’re going to discuss how anti-fraud tools can drive conversion rates and customer retention to improve the deployment ROI.

| Learning Points:

1. Why include humans in otherwise automated process flows (greater engagement helps secure faster purchase commitment and onboarding) 2. How all-in-one completion of contracts improves customer experience and reduces fraud 3. Cost drivers and the ROI of video-enabled solutions |

About this Session:

This session looks at the many options available to deliver a better customer experience in Smart Meetings and the positive financial impact it will make.

“Payback comes from Increased Business (higher completion ratio’s, more available time, broader reach, etc) plus Reduced & Avoided Costs”

Chris Jones, Managing Director, Icon UK Ltd

Topics include:

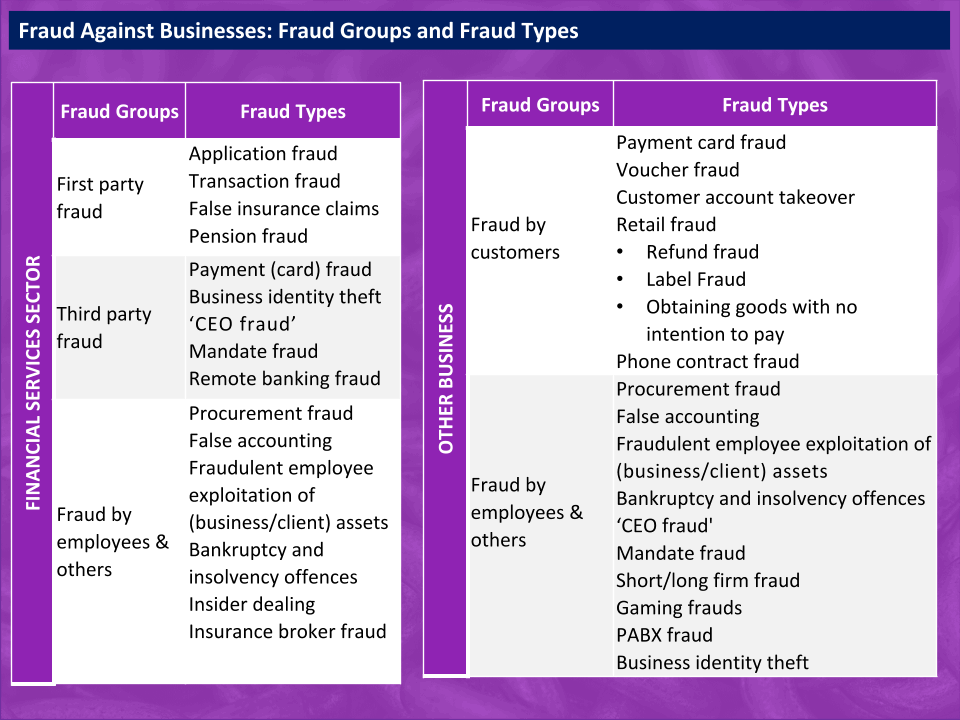

1. Different types of fraud add complexity to the challenge

The other videos in this series have discussed application fraud and identity theft in the context of online complex high value transactions, but there are many other types of fraud, for example:

Clearly, the solutions discussed will assist with many but not all fraud types. They target an important fast growing area where appropriately compliant, yet customer focused, technologies in widespread use are far from mature.

It is important to implement solutions that have a wide net and range of capabilities that can be flexibly deployed from within the same technical platform, rather than attempting to find point solutions for all types but, in turn, also multiplying internal complexity.

2. How can solutions reduce both fraud and improve outcomes more generally?

The technologies discussed in the previous videos can replace the physical meetings used by many professionals currently (eg, financial advisors, notaries, field sales staff, etc). They can be used for onboarding identification capture and a strong basis for ongoing authentication in almost all digital transactions. Because transactions can be completed in one session rather than days, it has been proved to reduce costs, deliver fast ROI and improve customer experience.

Are humans best equipped to detect fraudulent behaviour?

If you pick the right combination of technologies, it is possible to remove high-cost staff from certain types of transaction and let the customers serve themselves. However, the more complex and regulated the transaction, the more challenging that becomes. So, when shouldn’t we completely automate?

Humans have high empathy in face-to-face situations, which is a driver of trust (particularly important for sensitive matters) and can manually integrate many different processes from different systems that have not yet been fully integrated. Humans are also good at detecting certain types of fraud, given the right points of comparison and supporting tools.

But humans are costly and can make mistakes easily, especially when they do not have the right tools or training. So, it’s all about the way in which technology is used to support business outcomes.

Ideally, humans should only be used for:

• Scheduled consultations in regular transactions for strong empathy and relationship building (e.g. financial advisory) or

• To assist step-up processes from a web and chat transaction for KYC or AML for example or

• Should be focused on the highest risk exception management in one-off transactions

How does all-in-one completion improve customer experience?

Wealthy individuals or millennials are time-poor and intolerant of mediocre processes, which leads to loss of engagement with the client every time a transaction stops for completion by a back-office function. Smart Meetings are:

• Convenient for all, removing the need to travel

• Documents can be completed and signed electronically, without all the signees being in the same location

• Time-efficient processes are favourably recognised by time-poor clients

3. What is the ROI of Smart Meeting platforms?

Payback comes from:

• Increased business through higher completion ratios, more available time or a broader geographic reach

• Reduced and avoided costs via less travel, paper, postage, scanning, follow-ups to obtain signed documents or paperwork, compliance checking

Consider a traditional financial advisor who travels around their region to meet potential and existing customers. The difference in process steps and productivity impact from changing just one trip to using digital technologies might look like this:

Analysis shows 10x ROI is common, with a payback period of months not years. Try the free ROI tool below.

4. What do the regulators think of digital change?

With this tremendous potential for full digital customer engagement management, productivity and cost-efficient client services, the regulators in many sectors are encouraging greater adoption of these technology types. Greater efficiencies help democratise access to expensive services (such as legal, financial advice, health, etc), which are currently recognised as serving only a fraction of the ideal population share. They also make UK organisations more competitive domestically and globally.

As an example, electronic documents and e-signatures have gained acceptance in many quarters but there is still too much paper, and many digital silo processes have breakouts for a separate signing process, including on paper. In the UK, the Law Commission’s review of the Electronic Execution of Documents and similar financial services industry reviews, shows there is an immediate impetus for change. Some previously perceived barriers, such as questions over the acceptability of e-signing, are now clearly shown to not be obstacles.

Having easily accessible, full and accurate records of all meetings could have saved big-time on PPI!

All this while simultaneously enabling faster and more customer convenient completion of onboarding, information requests, product insights and service. The target for every business to achieve this should not be 18-30 months, but just 2-6 months. The technologies and expertise to support this sort of change are available now.

| Take-aways: 1. Buy configurable platforms, don’t Build (your digital meeting capabilities) 2. Engage specialist providers (with a range of flexible tools and experience) 3. Rehumanise ‘Suitability to Service’ processes – enabling top & bottom-lines |

Bonus

Free ROI assessment

Why not try this simplified ROI calculator to see if your organisation would benefit from using Smart Meetings?

It only takes a few minutes to complete and will give you an idea how long implementing Smart Meetings will take to pay back.

Transform your and your Customer’s regulated Documents experience – ask how.

You must Login to access notes.

About the expert

Icon UK

Icon UK works with clients to unlock step-change cost reductions and business benefits from their Enterprise Document Management Infrastructure.

See more from Icon UK Visit icon-uk.net/index.html